Rate Review: Ensuring Affordability through Accountability

For decades, health insurance premiums skyrocketed alongside insurance industry profits. Left without a way to challenge these arbitrary hikes, consumers were stuck with larger bills without seeing improvements to their coverage. But, recently, state and national health reform initiatives have placed more power in the hands of consumers, creating new tools to hold insurance companies accountable. Rate review is one of those tools.

What is rate review?

Rate review is a process that requires insurance companies to open their books to ensure that they provide “accurate, verifiable data and realistic projections of health costs,” according to the nonpartisan Kaiser Family Foundation. Health Action New Mexico and our partner organizations worked to establish a rate review process to protect consumers and hold insurance companies accountable for unfair health care premium rate increases. The state enacted legislation on rate review in 2011. Now insurance companies have to justify rates with data and the state has to make these proposed increases public. Rate review works because it brings consumers into a process that was once conducted behind closed doors. It uses accountability to ensure affordability.

How does rate review work?

Insurance carriers must submit proposed rate increases to the New Mexico Office of the Superintendent of Insurance (OSI). OSI posts those rates on its website, where consumers can submit comments on the increases. Formal hearings can then be brought forth by consumers. Once OSI has heard from consumers and insurance carriers, it looks at each company’s financial data to determine whether the requests are valid. If a proposed rate is found to be backed by the evidence, the carrier must alter its proposal to an acceptable rate that matches the available data within 30 days.

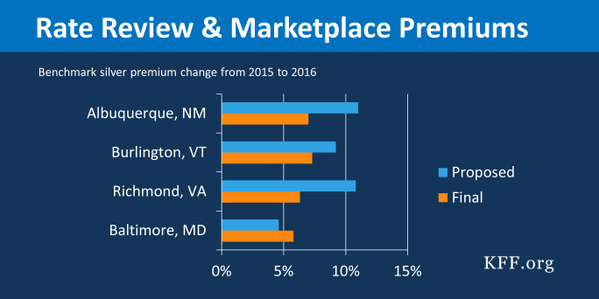

How has rate review affected premiums?

In many states, final rates are lower than proposed rates thanks to the rate review process. Kaiser Family Foundation recently found that rate review brought down overall rates across the state. Looking specifically at Albuquerque’s benchmark plan, the process directly reduced an increase in rates from 11 percent to 7 percent, saving money for consumers.

What’s the story with Blue Cross Blue Shield?

In June of 2015, Blue Cross Blue Shield (BCBS) of New Mexico proposed a whopping 51 percent rate increase. The request stunned consumers, the media, OSI - just about everybody. BCBS claimed that their customers required more expensive care than those enrolled in plans with other carriers. However, after carefully reviewing consumer feedback and BCBS’s financial information, OSI determined that the rate hike was far beyond justification.

The rates that BCBS chose to submit weren’t supported by the data the company provided. While OSI supported an increase of 24 percent – the highest among all carriers in the marketplace – BCBS refused to cooperate and, instead, dropped out of the market for 2016. This means thousands of consumers will need to find new coverage options in the health care marketplace. Fortunately, other insurance carriers are working to expand their networks to cover providers throughout the state.

What should I do if my BCBS plan is no longer available?

The first thing to keep in mind is that your current plan will remain active until January 1st, 2016. You have between November 1st and December 15th to sign up for a new plan that kicks in on January 1st. Four other insurance carriers offer plans on BeWellNM: New Mexico Health Connections, Molina, Presbyterian, and Christus St. Vincent. There will be 35 plans to choose from on BeWellNM, which is the only marketplace where financial help is available. OSI is also mobilizing a consumer roadshow to help those affected by BCBS’s exit from the marketplace. Click here to see when they are in a town near you.

BCBS does have a plan available but it will not be sold on BeWellNM and financial help will not be available. It is also a “Bronze” plan, meaning that it offers weak coverage with high out-of-pocket costs. Consumers should shop around on the exchange to find a plan that best meets their needs.

How can I get involved in rate review?

The next rate review process begins in the summer of 2016, when insurance carriers propose rates for 2017. Health Action New Mexico will be actively ensuring that consumers are representated as OSI considers the new rates. Submit your story to colin@healthactionnm.org if you think your premiums are being unfairly raised. Also be sure to submit comments to OSI next summer on this page. If you would like to request a hearing, call Health Action New Mexico and we will discuss the arrangements that need to be made to do so. Our number is (505) 322-2152.

Health Action